Interact Analysis 更新工业机器人预测:机器人类型、地区和行业差异较大

http://www.gkong.com 2024-12-20 16:47 来源:

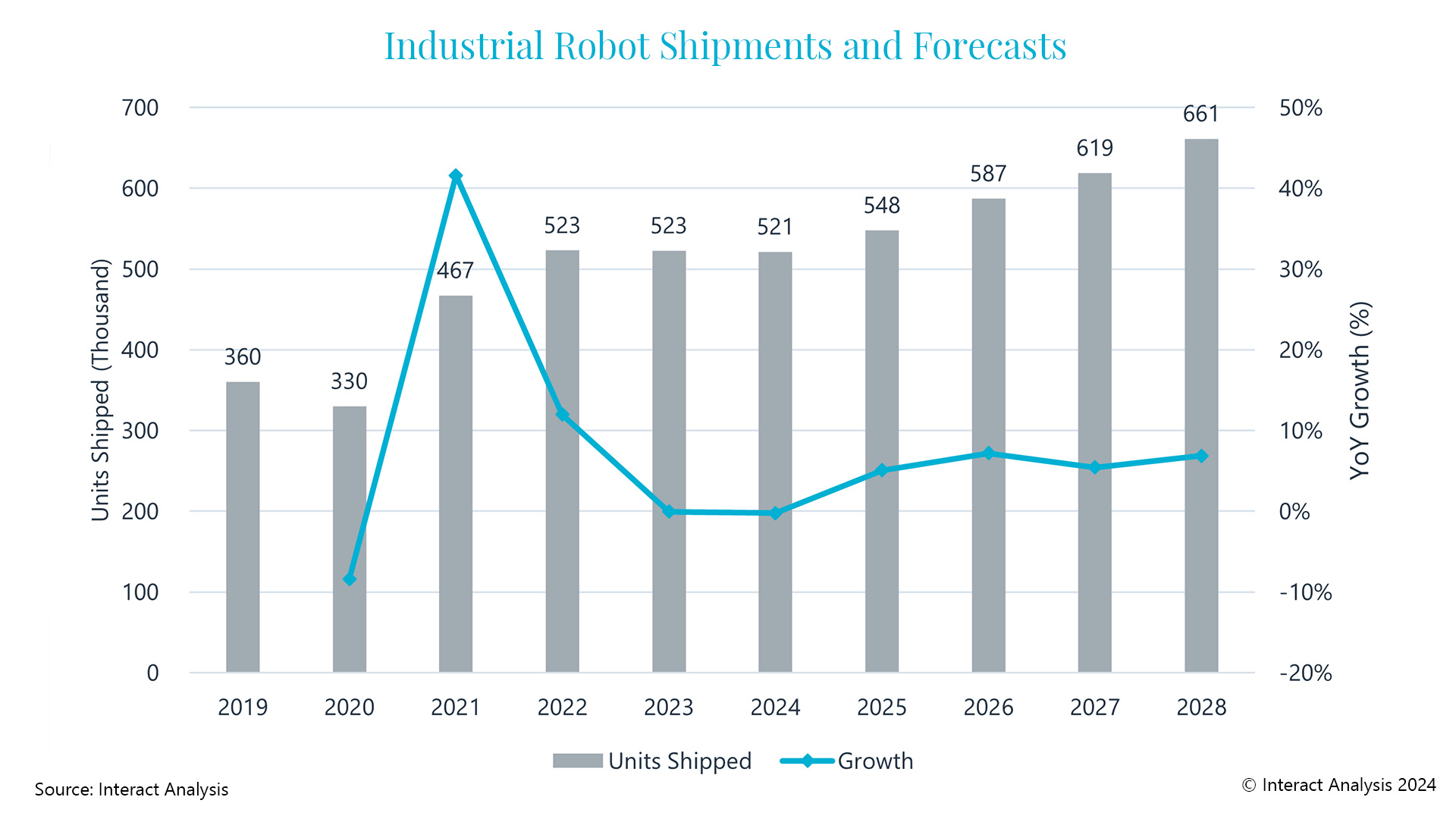

The industrial robot market is facing a mixed picture over the coming years, with 2024 set to end on a challenging note. Global robot shipments are projected to decline by 0.2%, following a flat performance in 2023. Compared with our May 2024 forecast, we have revised our 2024 projections for overall shipments downward by 5.8%; from over 553,000 units to 521,328 units. Additionally, the expected growth for 2025 has been reduced by 0.7 percentage points. These revisions reflect weaker-than-anticipated sales to the automotive industry in the second half of 2024 within the US and Europe, along with continued sluggish demand in China.

未来几年,工业机器人市场将面临喜忧参半的局面,2024 年将以充满挑战的方式结束。继 2023 年表现平平之后,全球机器人出货量预计将下降 0.2%。与 2024 年 5 月的预测相比,我们已将 2024 年的整体出货量预测下调了 5.8%;从超过 553,000 辆增加到 521,328 辆。此外,2025 年的预期增长率已下调 0.7 个百分点。这些修正反映了 2024 年下半年美国和欧洲汽车行业的销售额弱于预期,以及中国需求持续低迷。

Despite these challenges, we expect a gradual recovery in 2025. This is driven by anticipated increases in machinery investments – as key economies lower interest rates – alongside a broader recovery in the global manufacturing sector. However, factors such as high inventory levels and weak order intake are likely to persist in many industry sectors. This could potentially dampen robot demand during the first half of 2025. We forecast that industrial robot shipments will return to growth rates of over 7% by 2026.

尽管存在这些挑战,我们预计 2025 年将逐步复苏。这是由于主要经济体降低利率,预期机械投资将增加,同时全球制造业将全面复苏。然而,高库存水平和疲软的订单量等因素可能会在许多行业领域持续存在。这可能会抑制 2025 年上半年的机器人需求。我们预测,到 2026 年,工业机器人出货量将恢复到 7% 以上的增长率。

预计到2025年,全球机器人出货量将达到548,000台

Market by Robot Type:

按机器人分类市场:

Collaborative robots (cobots) stand out as a key growth area. We expect to see a 15.9% increase in shipments in 2024, despite the global economic slowdown. However, as competition increases, the price decline for cobots has been the most pronounced, resulting in a slower projected revenue growth rate of 11% during 2024.

协作机器人 (cobots) 是一个关键的增长领域。尽管全球经济放缓,我们预计 2024 年的出货量将增长 15.9%。然而,随着竞争的加剧,协作机器人的价格下降最为明显,导致 2024 年预计收入增长率将放缓至 11%。

SCARA robots are expected to see modest growth of 1.8% in 2024, fuelled by demand recovering in Asia’s semiconductor and electronics sectors. In contrast, other robot types will experience declines in shipments of 1-3% over the year, primarily due to challenges within the automotive and broader industrial sectors.

在亚洲半导体和电子行业需求复苏的推动下,预计 SCARA 机器人将在 2024 年实现 1.8% 的温和增长。相比之下,其他机器人类型的出货量将在一年内下降 1-3%,这主要是由于汽车和更广泛的工业部门面临的挑战。

Regional Market Dynamics:

区域市场动态:

Americas:

美洲

Robot shipments in the Americas are projected to contract by 6.6% in 2024, primarily due to sluggish demand from the automotive industry. Shipments in the electronics and metal sectors are also experiencing declines. While demand for robots in consumer-related sectors is growing, it is not enough to offset the downturn in other industries. However, the life sciences sector has been a bright spot, with strong growth in demand for robots used in pharmaceutical production and medical device assembly in the US.

预计到 2024 年,美洲的机器人出货量将收缩 6.6%,主要是由于汽车行业的需求低迷。电子和金属行业的出货量也在下降。虽然消费相关行业对机器人的需求不断增长,但这不足以抵消其他行业的低迷。然而,生命科学领域一直是一个亮点,美国对用于制药和医疗设备组装的机器人的需求强劲增长。

From 2024 to 2028, industrial robot shipments in the Americas are expected to grow at a CAGR of 6.1%. After the double-digit growth seen in 2021 and 2022, it is expected that the market will stabilize and expand at a more moderate pace in the coming years. We anticipate the continued trend towards greater automation and US reshoring initiatives will support the growth of manufacturing and demand for robots in the region.

从 2024 年到 2028 年,美洲的工业机器人出货量预计将以 6.1% 的复合年增长率增长。在 2021 年和 2022 年实现两位数增长之后,预计未来几年市场将稳定下来并以更温和的速度扩张。我们预计,自动化程度的持续趋势和美国的回流计划将支持该地区制造业的增长和对机器人的需求。

Asia Pacific:

亚太

In 2024, robot shipments in Asia Pacific are expected to increase by 2.3%, driven by a 3.3% increase in China and a 4.9% rise in the rest of APAC (excluding Japan and South Korea).

到 2024 年,亚太地区的机器人出货量预计将增长 2.3%,其中中国增长 3.3%,亚太地区其他地区(不包括日本和韩国)增长 4.9%。

- The Indian manufacturing industry continues to experience strong growth in 2024, spurred on by government investments in infrastructure. Industrial robots are rapidly gaining traction in India.

- The robot market in Taiwan and Southeast Asia is also seeing steady growth, fuelled by recovery of the semiconductor industry.

- China’s manufacturing sector is facing another challenging year in 2024. Due to overcapacity in the EV battery and solar panel industries, robot shipments in these sectors are expected to decrease by nearly 10%. Additionally, robot demand in the automotive and electronics sectors is expected to show only modest growth.

- 在政府对基础设施投资的刺激下,印度制造业在 2024 年将继续强劲增长。工业机器人在印度迅速受到关注。

- 在半导体行业复苏的推动下,台湾和东南亚的机器人市场也正在稳步增长。

- 2024 年,中国制造业将面临又一个充满挑战的一年。由于电动汽车电池和太阳能电池板行业的产能过剩,预计这些行业的机器人出货量将下降近 10%。此外,预计汽车和电子行业的机器人需求将仅出现适度增长。

From 2024 to 2028, robot shipments in Asia Pacific are projected to grow at a compound annual growth rate (CAGR) of 6.2%. Excluding China, South Korea and Japan, the region is expected to record a CAGR of 7.4%. Southeast Asian countries are emerging as key hubs for the electronics, semiconductor, and automotive industries, with international companies increasingly establishing factories there. This is expected to help drive robot demand.

从 2024 年到 2028 年,亚太地区的机器人出货量预计将以 6.2% 的复合年增长率 (CAGR) 增长。除中国、韩国和日本外,该地区的复合年增长率预计将达到 7.4%。东南亚国家正在成为电子、半导体和汽车行业的主要中心,越来越多的国际公司在那里建厂。预计这将有助于推动机器人需求。

Europe, Middle East and Africa (EMEA):

欧洲、中东和非洲

In 2024, robot shipments in EMEA are expected to decline by 9.2%. In Europe, orders sharply deteriorated in the second quarter, particularly in the automotive sector. Like North America, robot shipments in the European life sciences and food & beverage industries are expected to see smaller declines (2-3%), in contrast to the larger contractions anticipated in industries such as automotive, metal, and rubber & plastics. Although the new energy segment in Europe is comparatively small, it is also expected to experience a significant drop in robot shipments.

到 2024 年,欧洲、中东和非洲地区的机器人出货量预计将下降 9.2%。在欧洲,第二季度订单急剧恶化,尤其是汽车行业。像北美一样,欧洲生命科学和食品饮料行业的机器人出货量预计将出现较小的下降(2-3%),相比之下,汽车、金属、橡胶和塑料等行业预计会出现较大的收缩。尽管欧洲的新能源细分市场相对较小,但预计机器人出货量也将大幅下降。

From 2024 to 2028, we expect robot shipments in the EMEA region to grow at a CAGR of 5.6%. Demand growth in Eastern Europe is expected to accelerate with the expansion of the automotive supply chain in the region. Specialist countries in the life sciences sector, such as Denmark and Switzerland, are also expected to see above-average growth. However, larger manufacturing hubs, like Germany, are anticipated to experience slower growth, due to the ongoing recession in the manufacturing sector and structural challenges that could hinder economic recovery.

从 2024 年到 2028 年,我们预计欧洲、中东和非洲地区的机器人出货量将以 5.6% 的复合年增长率增长。随着该地区汽车供应链的扩张,预计东欧的需求增长将加速。预计丹麦和瑞士等生命科学领域的专业国家也将出现高于平均水平的增长。然而,由于制造业的持续衰退和可能阻碍经济复苏的结构性挑战,预计德国等较大的制造业中心将出现增长放缓。

In conclusion, the industrial robot market is navigating through a period of instability, with regional and sector-specific challenges influencing overall growth. While 2024 is a year of contraction, the medium-term outlook is more positive, especially as economic recovery gains momentum and new opportunities arise for automation.

总之,工业机器人市场正在经历一段不稳定时期,区域和特定行业的挑战影响了整体增长。虽然 2024 年是收缩之年,但中期前景更加乐观,尤其是在经济复苏势头增强和自动化新机遇出现的情况下。

编辑精选